Homeowners associations face federal and sometimes state tax obligations despite operating as community organizations rather than profit-seeking businesses. Your HOA's income and expenses trigger filing requirements that boards must understand and meet.

Most of an HOA's income supports community maintenance, but that doesn't exempt it from filing with the IRS. Here's what board members need to know about HOA taxes in 2025.

Why HOAs Pay Taxes

The IRS treats HOAs as taxable entities. While your community exists to maintain common areas and provide services rather than generate profits, the federal tax code doesn't exempt associations based on purpose alone.

However, HOAs often qualify for favorable tax treatment that significantly reduces or eliminates federal tax liability when structured correctly.

Two Tax Filing Options for HOAs

Your board chooses between two federal tax forms with very different requirements and tax implications.

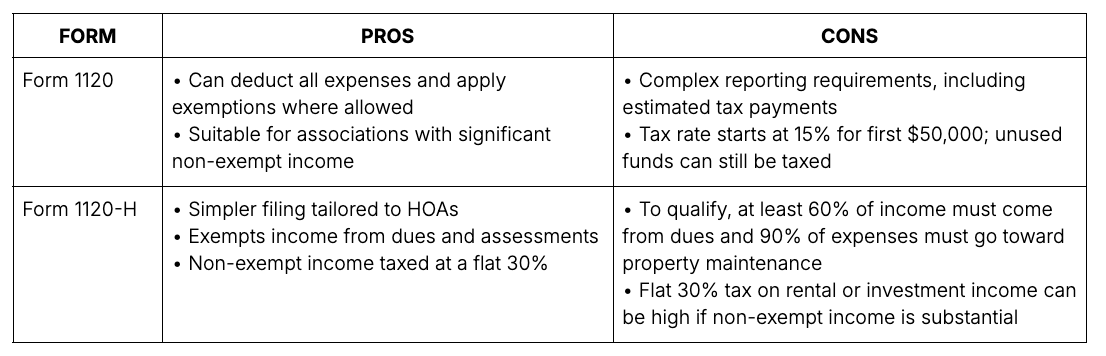

Form 1120: Standard Corporate Return

Form 1120 is the standard corporate tax return used by businesses nationwide. HOAs can file this form and pay taxes on net income after deducting legitimate business expenses.

This approach works when your HOA has substantial non-member income from sources like:

- Interest earnings on reserve accounts

- Rental income from cell towers or parking spaces

- Fees from non-residents using community amenities

Form 1120 allows full expense deductions but subjects net income to corporate tax rates.

Form 1120-H: HOA-Specific Return

Form 1120-H was designed specifically for homeowners associations that meet certain criteria. This specialized form offers significant advantages when your HOA qualifies.

The key benefit: Most income from member assessments qualifies as exempt income when your HOA meets 1120-H requirements. You pay tax only on non-exempt income like interest earnings or fee revenue.

The trade-off: Form 1120-H severely limits expense deductions. You get a flat deduction but can't itemize operating expenses.

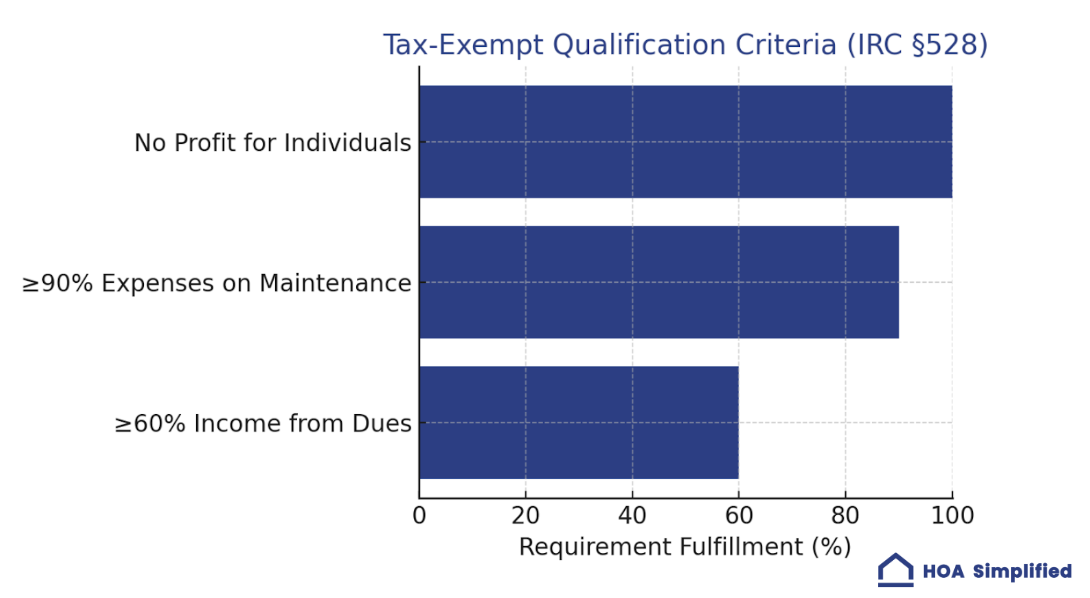

Qualifying for Form 1120-H Benefits

To file Form 1120-H, your HOA must meet these requirements:

- At least 60% of gross income must come from member assessments, fees, and dues

- At least 90% of annual expenditures must be for acquisition, construction, management, maintenance, and care of association property

- No members may be shareholders receiving profit distributions

Most traditional HOAs meet these criteria easily. The 60% income test excludes associations with substantial commercial revenue. The 90% expenditure test excludes organizations that distribute profits rather than maintain community property.

If you qualify, Form 1120-H typically produces lower tax liability than Form 1120 because member assessments receive exempt treatment.

Understanding Exempt vs. Taxable Income

The distinction between exempt and taxable income determines your community's tax obligation.

Exempt Income (When Filing 1120-H)

These income sources receive favorable treatment under Form 1120-H:

- Regular member assessments for operations and maintenance

- Special assessments for capital improvements or repairs

- Transfer fees paid by sellers during property transactions

- Late fees and interest on delinquent assessments

When these funds support community maintenance and improvements, they qualify as exempt income that doesn't trigger federal tax liability.

Taxable Income

These income sources face taxation regardless of which form you file:

- Interest earnings from savings accounts or reserve investments

- Rental income from cell towers, parking, or amenity rentals

- Fees from non-members using community facilities

- Vendor rebates or commission payments

Even when filing 1120-H, these sources produce taxable income subject to federal tax.

Need help with HOA tax preparation? Get Expert Assistance

Critical Filing Deadlines

HOA tax returns follow different deadlines based on your fiscal year structure.

Calendar Year HOAs (January 1 - December 31)

If your fiscal year matches the calendar year, your federal return is due April 15 following the tax year. Your 2024 return was due April 15, 2025.

Fiscal Year HOAs (Other 12-Month Periods)

Many HOAs use fiscal years ending June 30 to align with budget cycles. These associations file by September 15 following fiscal year end.

Extensions are available when you can't meet original deadlines, but extensions delay filing, not payment. Estimated tax payments may be required to avoid penalties.

State Tax Obligations

Federal returns aren't your only obligation. Many states impose separate tax or filing requirements on HOAs:

- California requires corporations, including HOAs, to file annual returns and pay minimum franchise taxes

- Florida has no state income tax, simplifying obligations for HOAs operating there

- Texas has no corporate income tax but may require franchise tax filings

- Other states have varied requirements

Research your state's specific rules or engage tax professionals familiar with HOA obligations in your jurisdiction.

Common Tax Filing Mistakes

Several errors regularly create problems for self-managed HOAs:

Missing the Deadline

Late filing triggers penalties that compound daily. Calendar deadlines and file early to avoid late penalties.

Choosing the Wrong Form

Filing 1120 when 1120-H would produce lower tax liability costs your community money unnecessarily. Evaluate which form produces better results annually.

Misclassifying Income

Treating taxable income as exempt or vice versa creates audit risk and potential penalties. Understand classification rules or get professional guidance.

Inadequate Documentation

Tax returns require supporting documentation: financial statements, income records, expense tracking, and board resolutions. Maintain organized records that support filed returns.

Forgetting 1099 Requirements

When your HOA pays contractors $600 or more annually, you must issue 1099 forms by January 31 and file copies with the IRS. Missing 1099 deadlines triggers separate penalties.

The Professional Tax Preparation Advantage

HOA tax rules are complex and specialized. General accountants who primarily serve individuals or conventional businesses may lack HOA-specific expertise.

Professional HOA tax services provide:

Form selection analysis that determines whether 1120 or 1120-H produces better results for your community

Income classification that correctly identifies exempt and taxable sources

Deadline tracking that ensures timely filing of federal returns, state returns, and 1099 forms

Audit support if the IRS questions filed returns or requests additional documentation

Multi-year planning that structures operations to minimize long-term tax obligations

The cost of professional preparation typically saves more than it costs through optimized filing approaches and avoided penalties.

Building Systems for Annual Compliance

Tax preparation becomes easier when your community maintains organized records year-round:

Monthly financial statements provide clean data for year-end tax preparation

Income source tracking distinguishes exempt member assessments from taxable interest or fee income

Vendor payment records identify contractors requiring 1099 forms

Board resolutions document decisions about special assessments or fee structures

Prior year returns serve as reference points for consistent filing approaches

Start preparing for next year's return now by establishing systematic recordkeeping.

The Bottom Line on HOA Taxes

Federal tax obligations are real, deadlines are firm, and penalties for non-compliance are substantial. But favorable treatment is available when you understand HOA-specific rules and file correctly.

Your community might pay minimal federal taxes or none at all when:

- You qualify for Form 1120-H treatment

- Most income comes from member assessments

- Taxable income sources remain minimal

Proper preparation, accurate form completion, and deadline adherence prevent compliance issues while reducing financial burden on your community.

Don't let tax obligations become a crisis. Build systems that make annual filing routine rather than stressful.