Few topics generate more anxiety among homeowners than a special assessment. The prospect of an unexpected bill, sometimes for thousands of dollars, naturally creates concern and pushback. For boards, the decision to levy a special assessment is rarely taken lightly. It usually means something went wrong with planning, or an emergency arose that no amount of planning could have prevented.

Understanding what special assessments are, when they are appropriate, and what alternatives exist helps boards make better financial decisions and communicate them effectively to homeowners.

What Is a Special Assessment and Why Does It Happen?

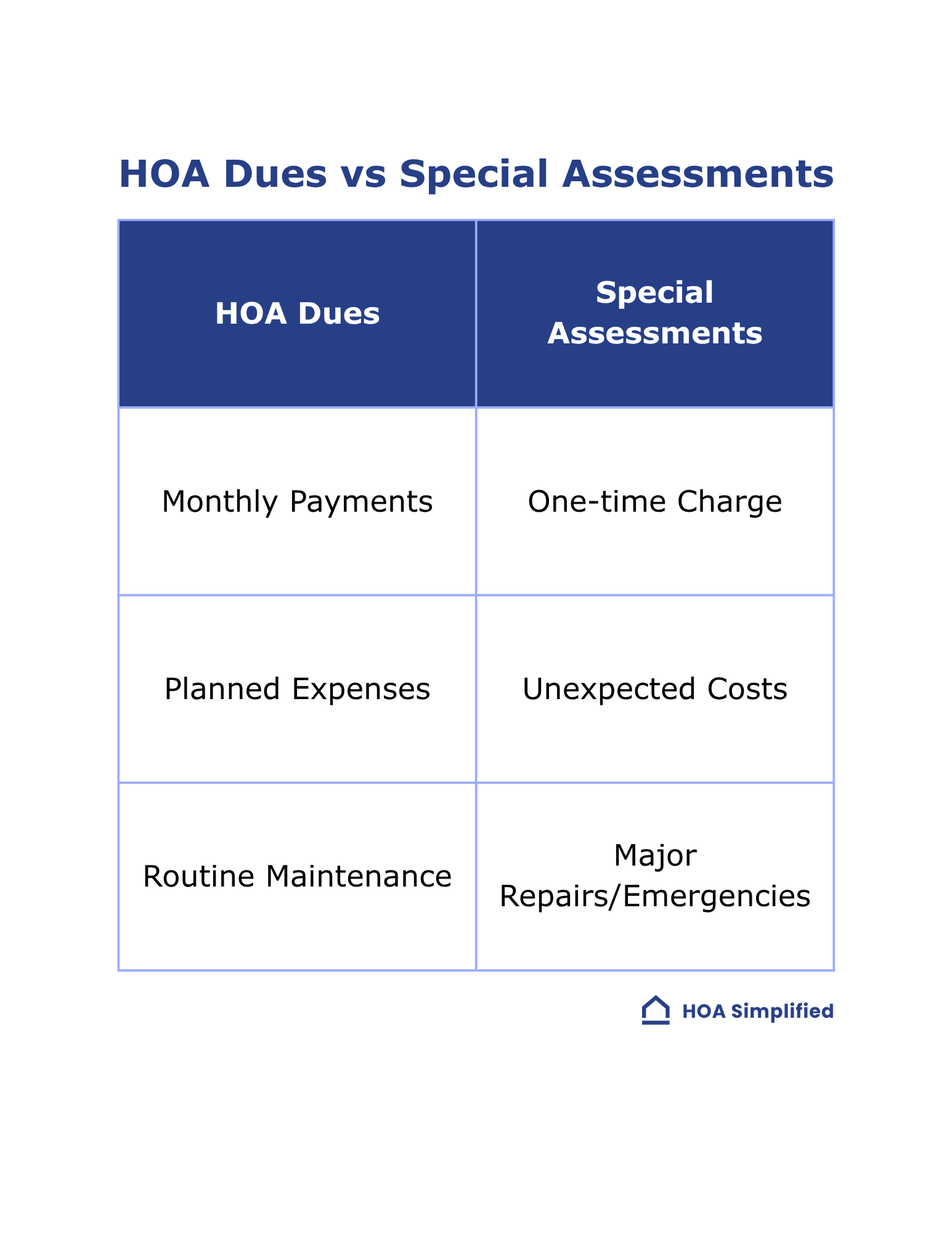

A special assessment is a one-time charge levied on all homeowners in addition to regular monthly or quarterly assessments. Unlike regular assessments that fund ongoing operations and reserve contributions, special assessments address specific capital needs that existing funds cannot cover.

Common triggers include unexpected major repairs (a failed roof system, structural damage from water intrusion, or emergency plumbing replacement), reserve fund shortfalls that accumulated over years of underfunding, mandatory compliance work required by building codes, and natural disaster damage not fully covered by insurance.

Voting Requirements Under California Law

California Civil Code Section 5605 sets clear thresholds for when a special assessment requires homeowner approval. Exceeding them without a proper vote exposes the association to legal challenge.

Without a membership vote, the board may levy a special assessment up to 5% of the association's budgeted gross expenses for that fiscal year. For an association with a $500,000 annual budget, that means the board can approve up to $25,000 on its own authority.

With a membership vote, any special assessment exceeding the 5% threshold requires approval by a majority of a quorum of the membership. The only exception is an emergency necessitated by circumstances that could not reasonably have been foreseen and that require immediate action (such as a court-ordered repair or an imminent safety hazard).

Ready to simplify your HOA? Request a Proposal

Member Notice and Approval Procedures

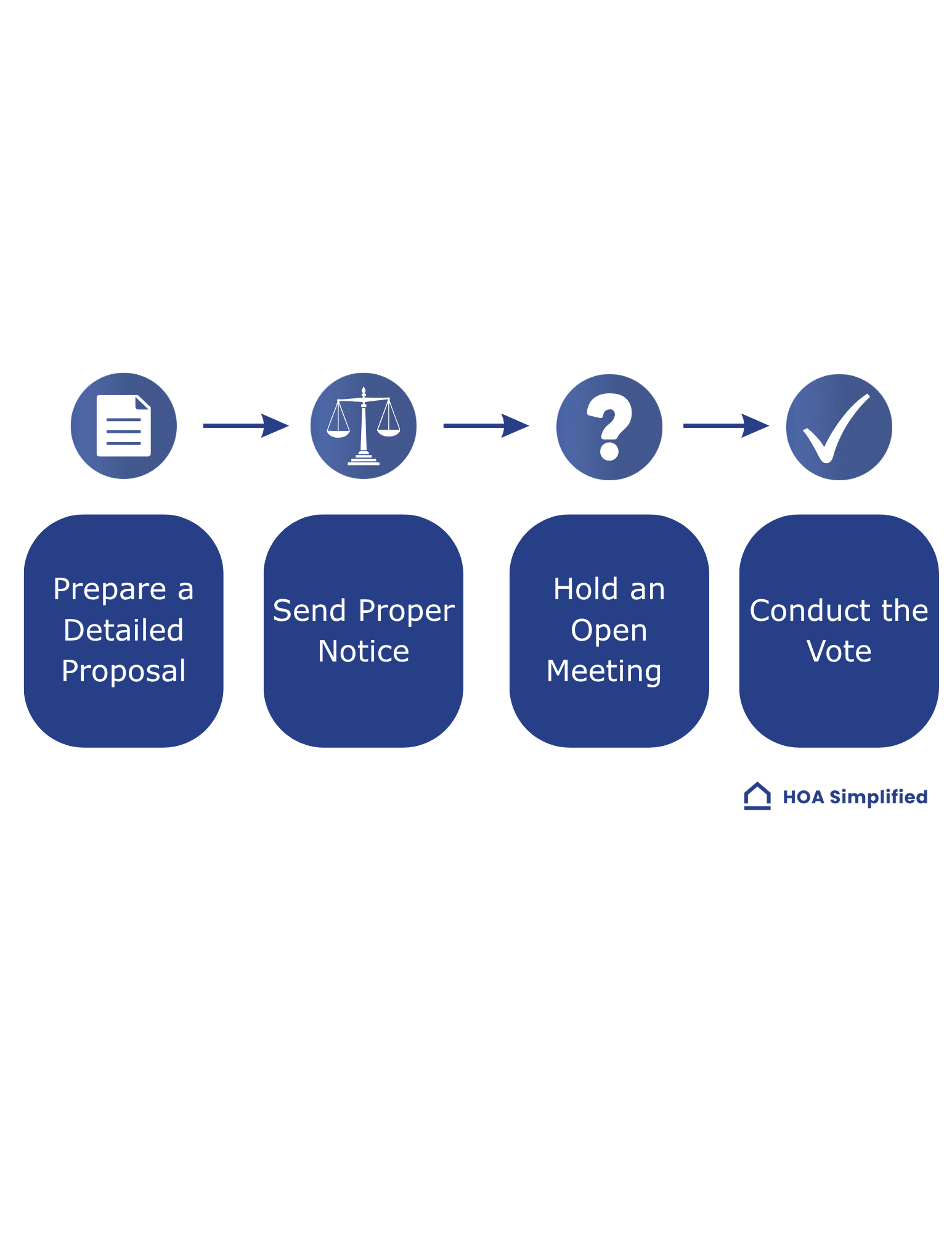

When a special assessment requires a membership vote, the board must follow specific procedural steps.

Prepare a detailed proposal. Draft a written document explaining the need, the total amount, how the per-unit share was calculated, and the payment timeline. Include supporting materials such as contractor bids, engineering reports, or reserve study findings.

Send proper notice. California law requires notice of any meeting at which a special assessment will be voted on to be delivered at least 10 to 90 days before the meeting, depending on the type of vote.

Hold an open meeting. Present the proposal and allow homeowners to ask questions. A well-prepared board that provides clear answers builds credibility, even when the news is unwelcome.

Conduct the vote. Follow your governing documents and state election procedures. Ballots must be handled according to California's secret ballot requirements under Civil Code Section 5100.

How to Calculate the Right Amount

Setting the correct amount requires careful analysis. Underestimating forces the board to levy a second assessment. Overestimating creates a surplus and raises questions about the board's judgment.

Start with actual project costs based on competitive bids from qualified contractors. Add a contingency of 10% to 15% for unforeseen conditions, particularly on older buildings where hidden problems commonly surface during construction. Factor in project management fees, legal costs, and required permits.

Divide the total according to your governing documents' allocation formula. Many associations allocate by unit size or percentage of interest rather than equally. Review your CC&Rs to confirm the correct method before calculating individual shares.

Alternatives to Special Assessments

Before levying a special assessment, boards should evaluate other funding options.

Adequate reserve funding is the best long-term prevention. Associations that follow their reserve study's recommended annual contribution rarely face special assessments. If reserves are underfunded, increasing contributions over three to five years can close the gap without a sudden one-time charge.

HOA loans spread costs over time, converting a large lump sum into smaller monthly payments funded through a modest assessment increase. This works well when homeowners would face genuine hardship paying a special assessment in full.

Phased project execution breaks large capital projects into stages. The board addresses the most urgent buildings first and phases remaining work over two or three budget cycles.

Insurance recovery should be explored when damage results from a covered event. Review your policy thoroughly before assuming the community must self-fund repairs.

Communicating With Homeowners

How the board communicates a special assessment matters almost as much as the assessment itself.

Be transparent about the need. Show the engineering report, the contractor bids, or the reserve study findings that demonstrate the funding gap. Homeowners who understand the problem are more likely to accept the solution.

Acknowledge the burden. Don't minimize it. Explain what alternatives were considered before arriving at this recommendation.

Offer payment options. When possible, allow homeowners to pay in installments over 6 to 12 months rather than requiring a single lump sum. This flexibility reduces delinquency rates and shows the board is working with homeowners, not against them.

Follow up after the project. Share results with the community. A summary of costs versus budget and what the investment means for long-term community health reinforces the board's credibility.

Common Mistakes Boards Make

Waiting too long to act. Deferring necessary repairs to avoid a difficult conversation almost always increases the eventual cost. Water damage spreads, structural issues worsen, and what could have been a $200,000 repair becomes a $500,000 emergency.

Skipping the alternatives analysis. Boards that jump straight to a special assessment without evaluating loans, phased approaches, or reserve reallocation miss opportunities to reduce homeowner burden.

Inadequate project scoping. Levying a special assessment based on a rough estimate rather than detailed bids leads to cost overruns. Invest in proper scoping before setting the amount.

Failing to follow legal procedures. Procedural shortcuts in notice requirements, voting thresholds, or meeting rules can invalidate a special assessment entirely. When in doubt, consult your association's attorney before proceeding.

Special assessments are a necessary tool in community association management. When they are properly planned, legally sound, and clearly communicated, homeowners may not welcome the expense, but they can understand and respect the board's decision.