Property damage happens. Storms cause roof leaks, pipes burst and flood units, tree branches fall on cars. When damage occurs in an HOA community, the first question everyone asks is: who pays for this?

The answer isn't always simple. Responsibility depends on where the damage occurred, what caused it, and what your governing documents say. Here's what you need to know.

Understanding the Basic Framework

Most HOA responsibility follows a clear principle: homeowners handle everything inside their unit, the association handles common areas and building exteriors.

Your governing documents spell out exactly where that line falls. CC&Rs typically define common areas, limited common areas, and individual unit boundaries. These definitions determine who handles repairs.

In a typical townhouse or condo community, the HOA owns and maintains building exteriors, roofs, landscaping, parking lots, and amenities like pools or clubhouses. Homeowners own and maintain everything inside their unit walls.

The specifics vary by community, so reviewing your documents is essential before assuming who's responsible.

When the HOA Is Responsible

The association must repair damage to common areas and building elements it's required to maintain.

If a storm damages the roof and water leaks into your unit, the HOA handles roof repairs. If poor drainage causes foundation issues affecting multiple units, that's an association responsibility. If tree roots from common area landscaping damage a sewer line, the HOA pays. The key factor is location and ownership. If the damaged element is part of what the HOA maintains, they're responsible for fixing it.

This responsibility extends to damage caused by HOA negligence. If the association failed to maintain common area plumbing and a pipe bursts, flooding your unit, they're liable for repairs to your property as well as the plumbing itself.

When Homeowners Are Responsible

Homeowners handle damage to their individual units and any elements they own.

If your water heater fails and floods your bathroom, you pay for repairs. If you accidentally damage a wall during renovations, that's your responsibility. If your plumbing leaks and damages your downstairs neighbor's ceiling, your insurance typically covers it.

Damage you cause to common areas is also your responsibility. If you back into the clubhouse wall, you pay for repairs. If your guest breaks equipment in the fitness center, you're liable.

The Gray Areas

Some situations aren't clear-cut. These require careful review of your documents and potentially legal advice.

Shared walls: If a pipe inside a shared wall leaks, who's responsible? This depends on your CC&Rs definition of boundaries and maintenance responsibilities.

Limited common areas: These are common areas assigned to specific units, like patios or balconies. Your documents specify whether the HOA or homeowner maintains them.

Building systems: If a central HVAC system serves multiple units but has individual thermostats, responsibility for repairs might be split depending on what component failed.

When responsibility is unclear, the board should consult your attorney rather than guessing.

Steps to Take After Damage Occurs

Document everything immediately. Take photos and videos of all damage before anyone starts cleanup or repairs.

Contact your insurance company promptly if you believe your policy covers the damage. Most policies have reporting deadlines. Missing them can jeopardize your claim.

If you think the HOA is responsible, notify the board or property manager in writing right away. Include your documentation and a clear description of what happened.

Need professional HOA support? Request a Proposal

Don't start repairs without determining responsibility and getting approval. If you repair HOA-owned property without authorization, the association might not reimburse you. If the HOA starts repairs on your property, you might waive rights to file an insurance claim or lawsuit.

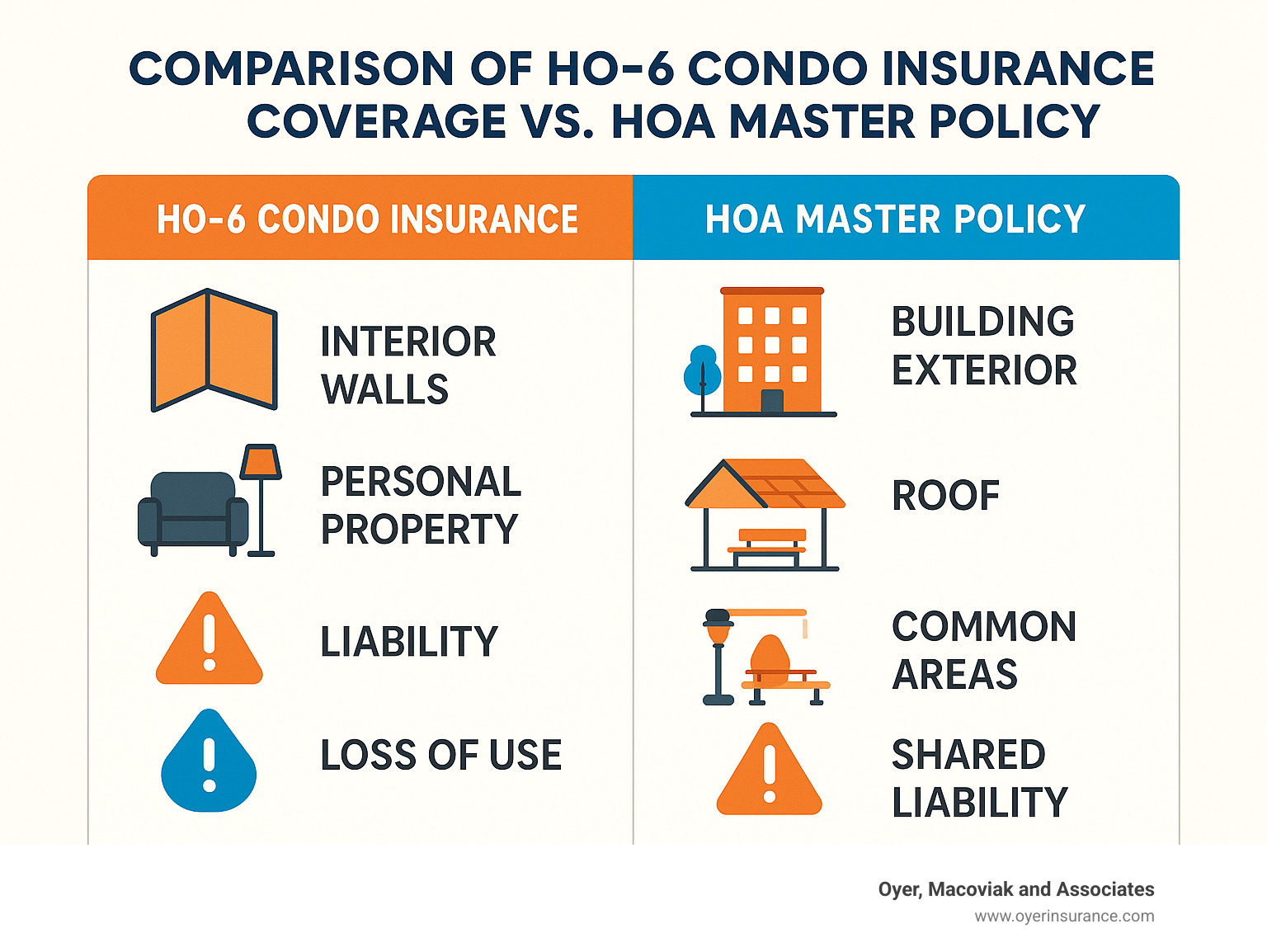

Insurance Considerations

HOAs typically carry master policies covering common areas and building exteriors. These policies often include liability coverage for injuries on common property.

Homeowners need their own HO-6 (condo) or HO-3 (single-family home) policies covering unit interiors, personal property, and liability. These policies should include loss assessment coverage, which pays your share if the HOA's insurance doesn't fully cover a claim.

After major damage, both the HOA and affected homeowners should file claims with their respective insurers. The insurance companies will determine coverage and coordinate payment.

Never assume the HOA's insurance covers damage to your unit contents or interior improvements. It doesn't. You need your own policy.

Preventing Disputes

Clear communication prevents most damage-related disputes. HOA boards should educate homeowners about maintenance responsibilities before problems occur.

Include a summary of repair responsibilities in new homeowner packets. Post information on your community website. Send periodic reminders about common confusion points.

When damage happens, respond quickly. Acknowledge receipt of homeowner notifications. Investigate promptly. Communicate your findings and next steps.

If the HOA is responsible, make repairs as quickly as possible. If the homeowner is responsible, explain why clearly and reference the specific sections of your CC&Rs that support that determination.

When Negligence Is Involved

HOA negligence creates legal liability. If the board knew about a maintenance problem, failed to address it, and that failure caused damage, the association is responsible even if the damaged item would normally be a homeowner's responsibility.

For example, if homeowners repeatedly reported water intrusion through a roof but the board delayed repairs, and units suffered water damage as a result, the HOA is liable for interior damage as well as roof repairs.

Document all maintenance requests and board responses. If you're a homeowner, keep copies of every notice you send about maintenance concerns. If you're a board member, ensure your records show timely response to homeowner complaints.

Special Assessments for Major Damage

When damage to common areas exceeds insurance coverage or reserve funds, boards may need to levy special assessments.

This requires proper notice and often a vote, depending on your state law and bylaws. Boards can't just bill homeowners without following proper procedures.

Before imposing an assessment, explore other options. Can the repair be phased over multiple years? Can you secure a loan? Are there insurance proceeds you haven't collected?

Special assessments are sometimes necessary, but they should be the last resort after exhausting alternatives.

The Bottom Line

Property damage responsibility in HOA communities depends on location, cause, and your governing documents.

Document damage immediately. Notify the appropriate party in writing. File insurance claims promptly. Don't start repairs until responsibility is determined.

Clear communication and proactive maintenance prevent most disputes. When disagreements occur, refer to your CC&Rs and seek legal advice if needed.

Understanding responsibility before damage happens saves time, money, and conflict when it inevitably occurs.