HOA loans provide associations with strategic financing for major capital projects. Understanding when and how to use lending products helps boards make informed decisions about community investments.

What Is an HOA Loan?

An HOA loan is financing taken out by the association itself, not individual homeowners. The association borrows funds for major community expenses and repays the loan using future assessment income.

Unlike personal mortgages, HOA loans typically use the association's right to collect assessments as collateral rather than physical property. This structure allows associations to access capital without placing liens on individual units.

When Borrowing Makes Financial Sense

HOA loans serve specific purposes beyond emergency funding. Three scenarios favor association borrowing over special assessments.

First, reserves prove insufficient when urgent repairs arise. A failed roof or plumbing system cannot wait for reserve accumulation. Immediate financing prevents further damage and liability.

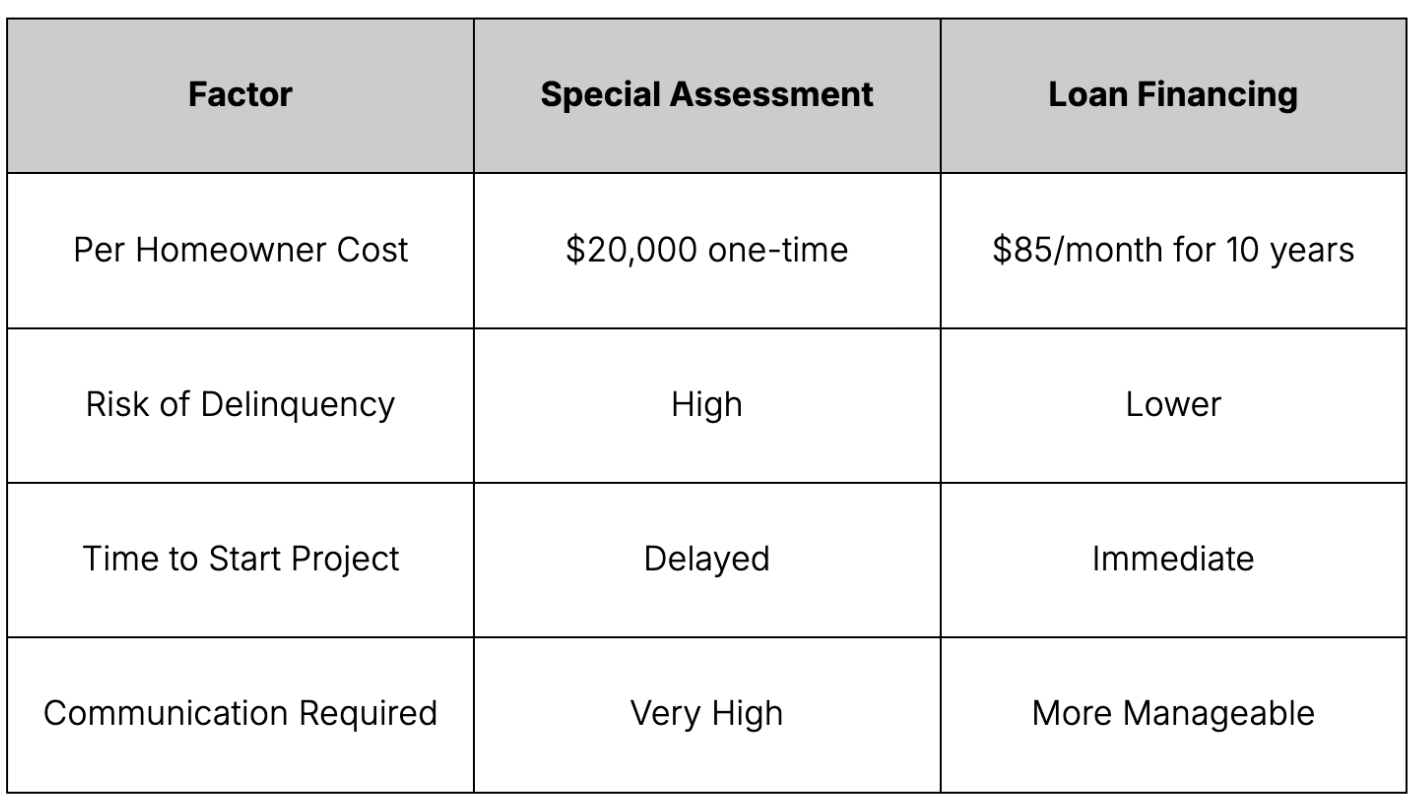

Second, spreading costs over time reduces homeowner burden. A $500,000 repair translates to a manageable monthly increase rather than a $5,000 per-unit special assessment. This approach maintains community stability and reduces delinquency risk.

Third, project timing creates savings. Completing work during contractor off-seasons or bundling multiple projects often yields significant discounts. Financing enables associations to capitalize on favorable market conditions.

Ready to simplify your HOA? Request a Proposal

How Lenders Evaluate HOA Applications

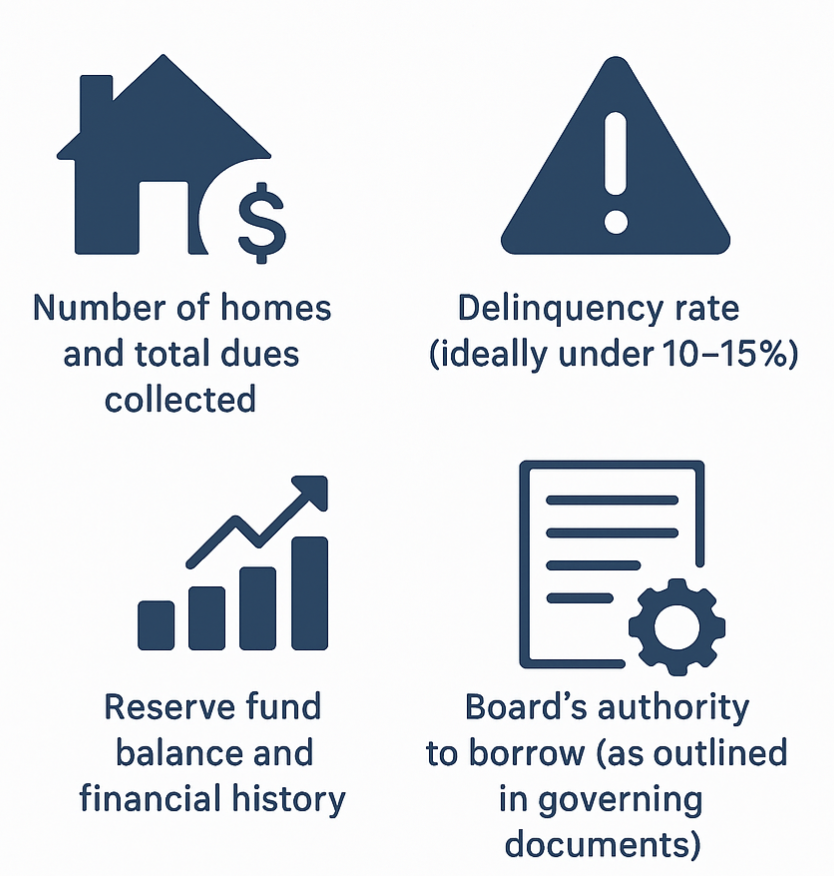

Financial institutions assess HOA creditworthiness differently than individual borrowers. Lenders examine several key factors before approving association loans.

Reserve fund health indicates financial stability. Lenders prefer associations with established reserve accounts and regular contributions. Strong reserves demonstrate fiscal responsibility and repayment capacity.

Collection rates matter significantly. High delinquency percentages signal potential repayment problems. Lenders typically require collection rates above 90% and may reject applications from associations with chronic collection issues.

Budget adequacy affects approval decisions. Lenders review operating budgets to ensure existing assessments cover current expenses plus proposed loan payments. Associations cannot leverage future assessment increases unless governing documents allow them.

Insurance coverage protects lender interests. Adequate property and liability insurance ensures repairs maintain collateral value. Lenders often require specific coverage levels as loan conditions.

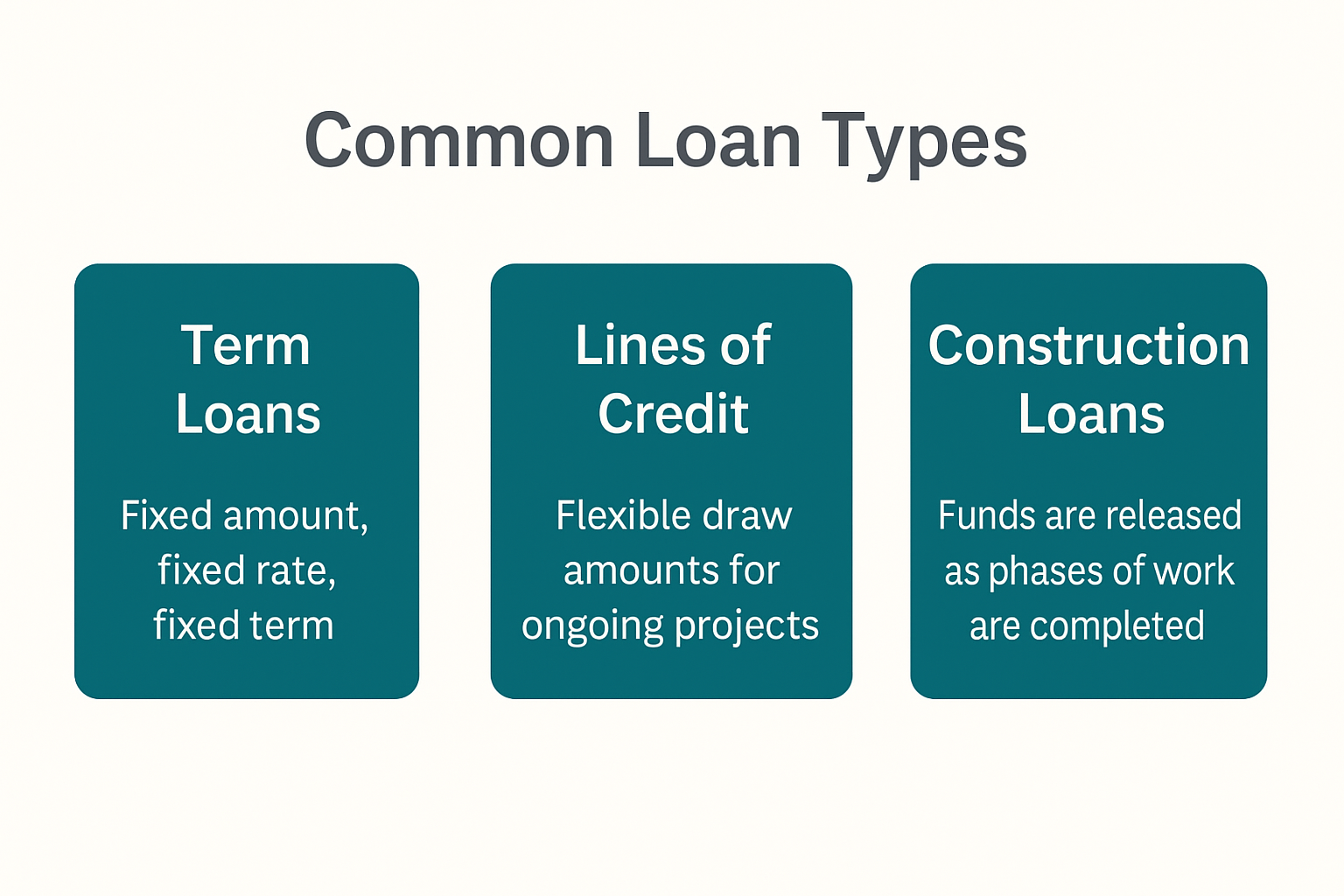

Loan Terms and Structure

HOA loans typically span 3 to 15 years depending on project scope and association finances. Shorter terms minimize interest costs but require higher monthly payments. Longer terms reduce payment burden but increase total interest expense.

Interest rates reflect credit risk and market conditions. Well-managed associations with strong reserves secure favorable rates. Associations with financial challenges pay premium rates or face rejection.

Most HOA loans are unsecured, relying on assessment collection rights rather than property liens. This structure simplifies closing but may result in higher interest rates compared to secured financing.

Loan Approval Process

Board authorization represents the first requirement. Governing documents specify voting thresholds for borrowing decisions. Some require majority board approval while others mandate homeowner votes.

Review CC&Rs carefully before pursuing financing. Restrictions on borrowing authority or maximum debt levels may limit options. Amending governing documents takes time and may prove necessary.

Select lenders experienced with HOA structures. Traditional banks often lack expertise in association lending. Specialized lenders understand HOA governance and offer more flexible terms.

Prepare comprehensive financial documentation. Lenders require multiple years of financial statements, current budgets, reserve studies, and collection reports. Complete documentation accelerates approval and demonstrates professionalism.

Alternative Financing Considerations

Special assessments remain the traditional funding approach. One-time charges avoid interest costs and debt obligations. However, large assessments create hardship and collection challenges.

Reserve fund loans allow associations to borrow from their own reserves temporarily. This approach works for short-term needs but depletes funds for other projects. Repayment plans must not compromise future reserve adequacy.

Line of credit products provide flexible borrowing capacity. Associations draw funds as needed and pay interest only on outstanding balances. This structure suits projects with uncertain timing or phased construction.

Communication and Transparency

Homeowner communication proves essential when considering association debt. Board members should explain project necessity, financing terms, and payment impacts clearly.

Hold informational meetings before taking formal votes. Allow members to ask questions and voice concerns. Transparent communication builds trust and increases approval likelihood.

Document decisions thoroughly in meeting minutes. Record discussion points, vote results, and dissenting opinions. Proper documentation protects board members and demonstrates due diligence.

Making the Right Choice

HOA loans serve as valuable financial tools when used appropriately. They enable associations to address urgent needs, spread costs fairly, and capitalize on market opportunities.

However, borrowing creates obligations that affect future budgets. Boards must balance immediate needs against long-term financial health. Proper analysis and professional guidance ensure smart financing decisions.

Consider consulting with reserve specialists and financial advisors before committing to loans. Expert input helps boards evaluate alternatives and structure optimal financing solutions.