Every successful homeowners association runs on accurate, consistent accounting. But not all accounting methods work the same way, and the approach you choose directly impacts how clearly you understand your community's financial health.

Most board members aren't accountants. You're volunteers trying to make smart decisions with limited time and financial expertise. Understanding the three main accounting methods used by HOAs helps you choose the right approach for your community's size and complexity.

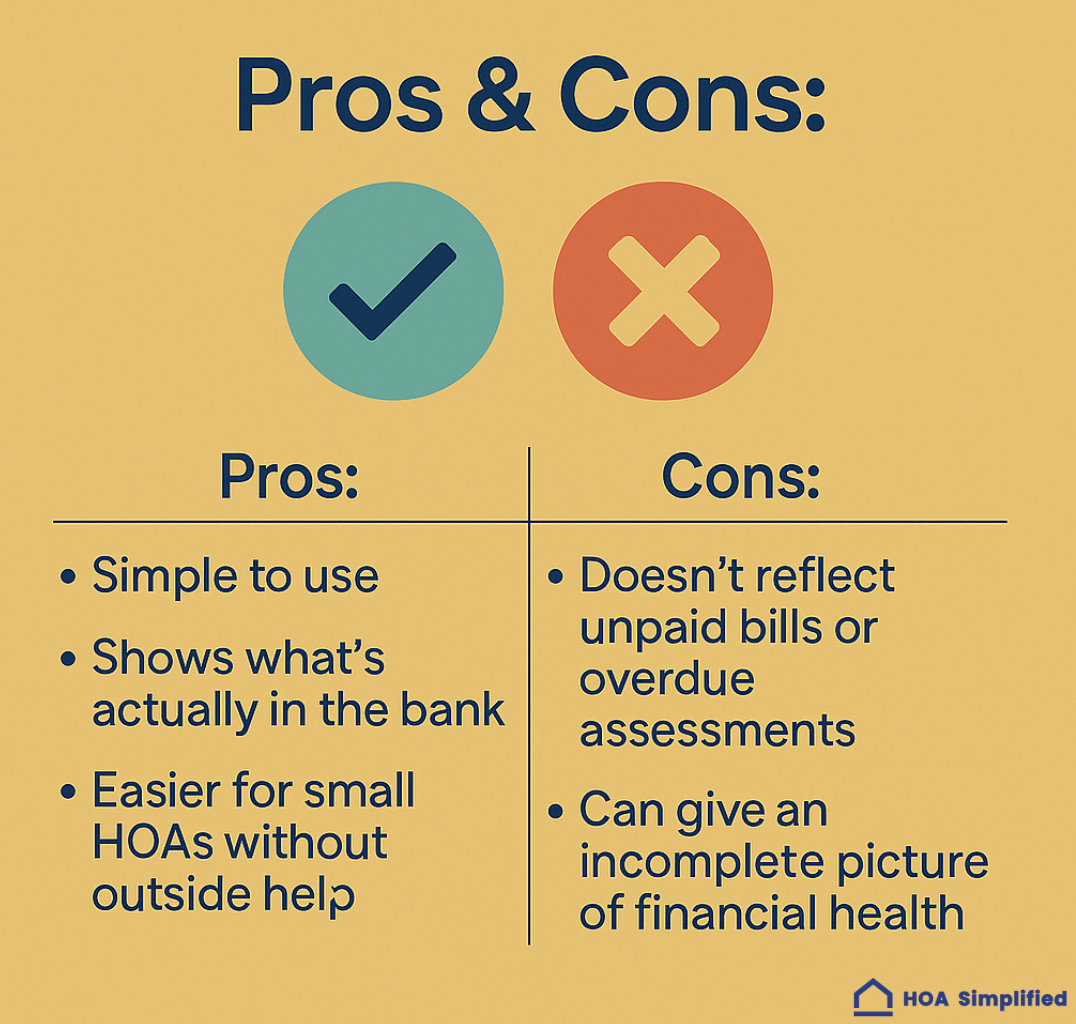

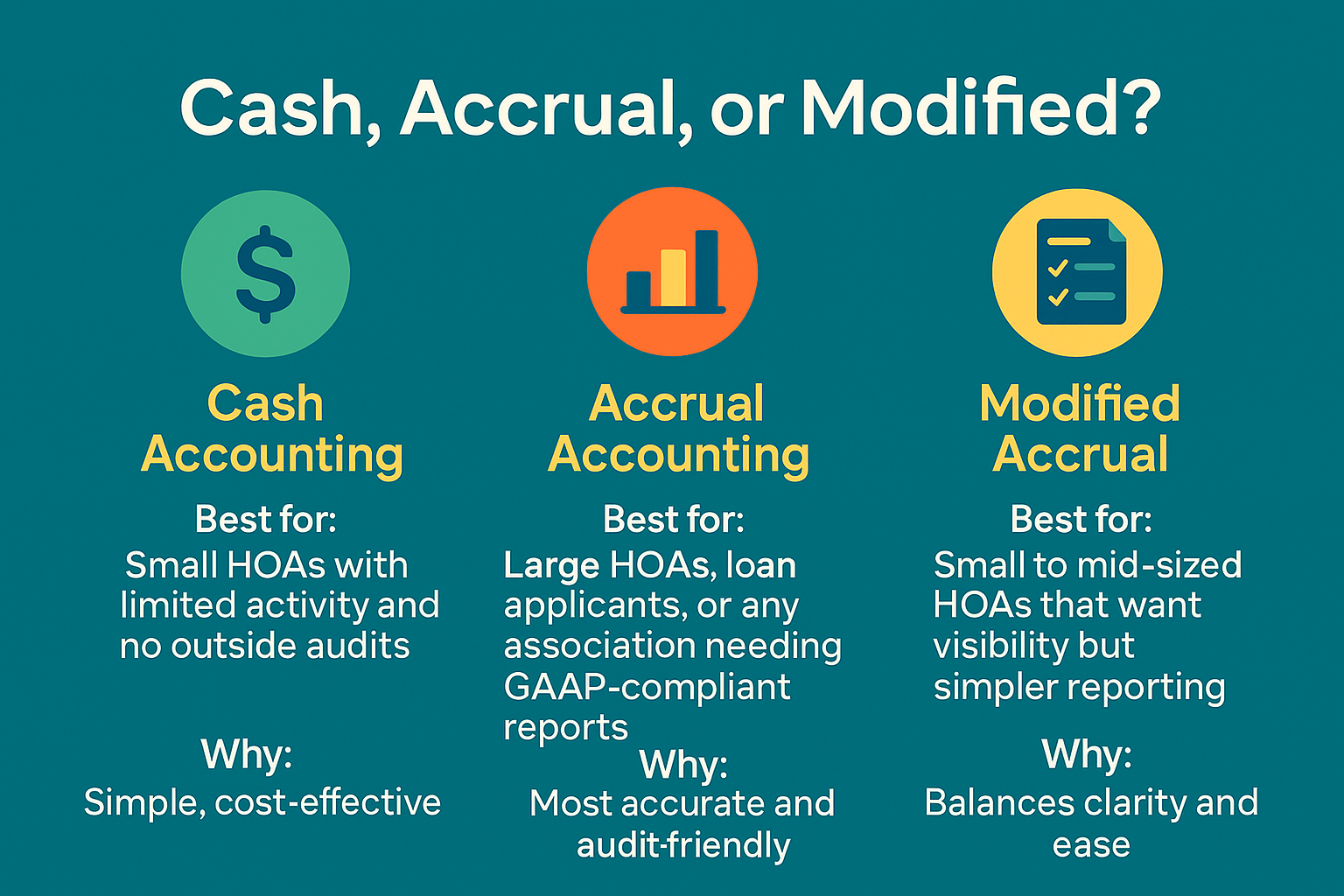

Cash Accounting: Simple and Straightforward

Cash accounting is exactly what it sounds like. You record income when money hits your bank account and expenses when you pay bills. Nothing gets documented until actual cash changes hands.

This method appeals to small HOAs for good reason. It's easy to understand, requires minimal bookkeeping effort, and gives you a clear picture of how much money you have right now.

Here's how it works in practice: homeowners pay March dues in early March, and you record that income in March. Your landscaping company sends an invoice in March but you don't pay until April, so the expense shows up in April's records.

For communities under 30 homes with straightforward finances, cash accounting often provides all the detail you need. Your financial reports match your bank statements, making it simple to track where your money actually is.

Ready to simplify your HOA? Request a Proposal

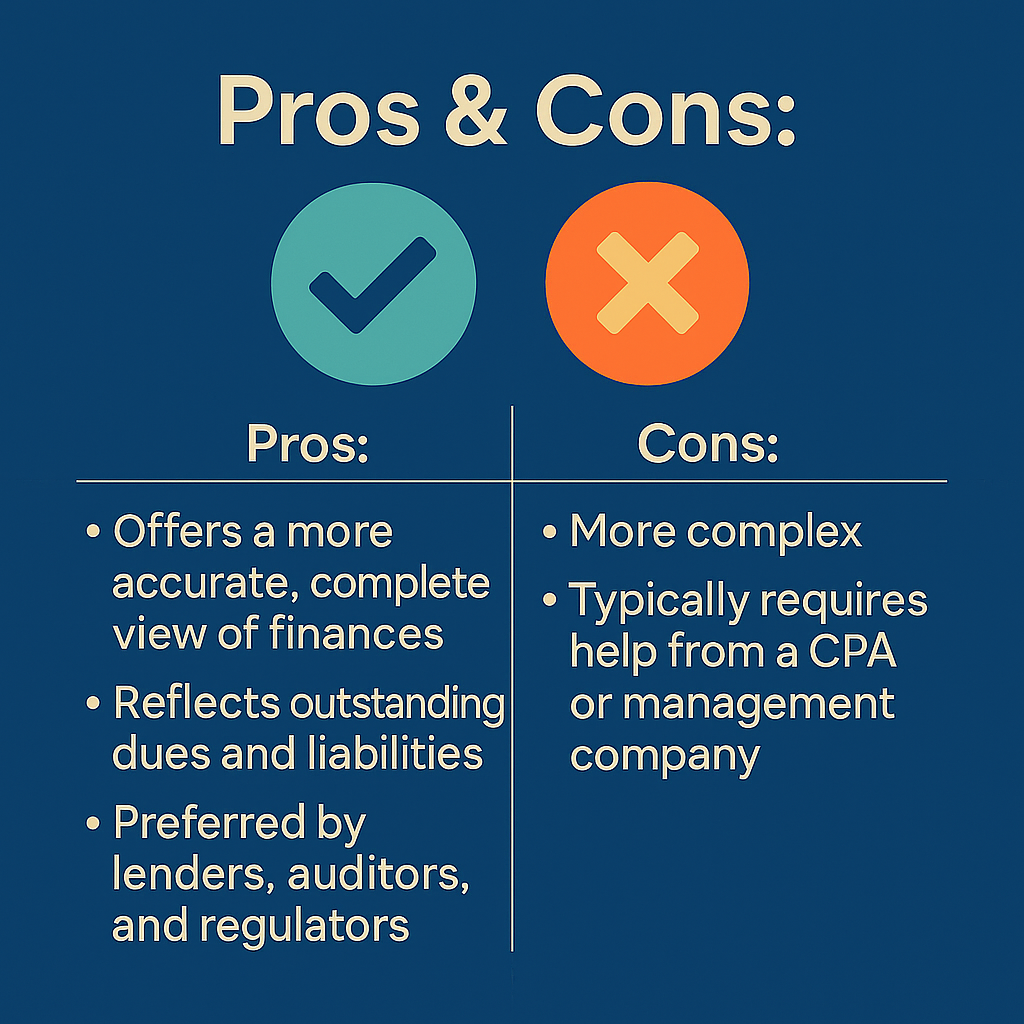

Accrual Accounting: A More Complete Picture

Accrual accounting takes a different approach. It records income when you earn it and expenses when you incur them, regardless of when cash actually moves.

This creates a more accurate view of your financial position. When homeowners owe March dues, you record that income in March even if some residents pay late. When your landscaper invoices you for March services, that expense appears in March even though you won't pay until April.

The advantage becomes clear when you're trying to understand your true financial situation. Cash accounting might show you're flush with money in March because everyone just paid dues, while masking the fact that you have significant bills coming. Accrual accounting reveals both sides of the equation simultaneously.

Medium to large HOAs typically need this level of detail. According to the Community Associations Institute, most communities over 50 homes use accrual or modified accrual methods because the financial complexity demands it.

Accrual accounting also becomes necessary when your HOA seeks loans, undergoes professional audits, or manages substantial reserve funds. Lenders and auditors expect to see the full financial picture that accrual methods provide.

Modified Accrual: The Middle Ground

Modified accrual combines elements of both approaches. It records income using the accrual method (when earned) but tracks expenses using the cash method (when paid).

This hybrid appeals to small and mid-sized HOAs looking for improved accuracy without full accrual complexity. You get a clearer view of expected income while keeping expense tracking simple and closely tied to your actual cash position.

Think of modified accrual as training wheels for associations growing into more sophisticated financial practices. It offers more insight than pure cash accounting without requiring the detailed tracking that full accrual demands.

Choosing the Right Method for Your Community

Here's a quick guide to help you decide:

Your HOA's size and financial complexity should drive this decision. Communities under 30 homes with simple budgets often do fine with cash accounting. The method matches how most people think about personal finances, making it accessible for volunteer boards.

As your community grows or takes on more complex financial obligations, accrual or modified accrual methods become worth the extra effort. They reveal financial trends earlier, support better planning, and provide the documentation that lenders and auditors require.

Consider switching to accrual accounting if your HOA:

- Manages significant reserve funds for long-term projects

- Seeks financing for major capital improvements

- Undergoes regular professional audits

- Struggles with homeowners who consistently pay late

- Needs more sophisticated financial forecasting

The transition isn't instant. You'll need to adjust your bookkeeping processes, possibly upgrade your accounting software, and help board members learn to read accrual-based financial statements.

Consistency Matters More Than Method

Here's what really counts: pick a method and stick with it. Switching between accounting approaches makes it nearly impossible to compare financial results year-over-year or identify meaningful trends.

Consistent methodology builds trust with homeowners. When your financial reports follow the same rules month after month, residents can actually understand what they're looking at and make informed judgments about board decisions.

Consistency also improves your own decision-making. You learn to read your financial statements accurately, spot problems early, and plan effectively when you're working with familiar data presented the same way each time.

Getting Professional Help

If you're unsure which accounting method fits your community, talk to a CPA familiar with HOA finances. The cost of a consultation is minimal compared to the financial clarity you'll gain.

Professional accountants can also handle the transition if you decide to switch methods. They'll ensure your financial records convert accurately and train your treasurer on the new approach.

Your accounting method forms the foundation of every financial decision your board makes. Choose wisely, stay consistent, and get expert guidance when you need it. Your community's financial health depends on it.